Short answer

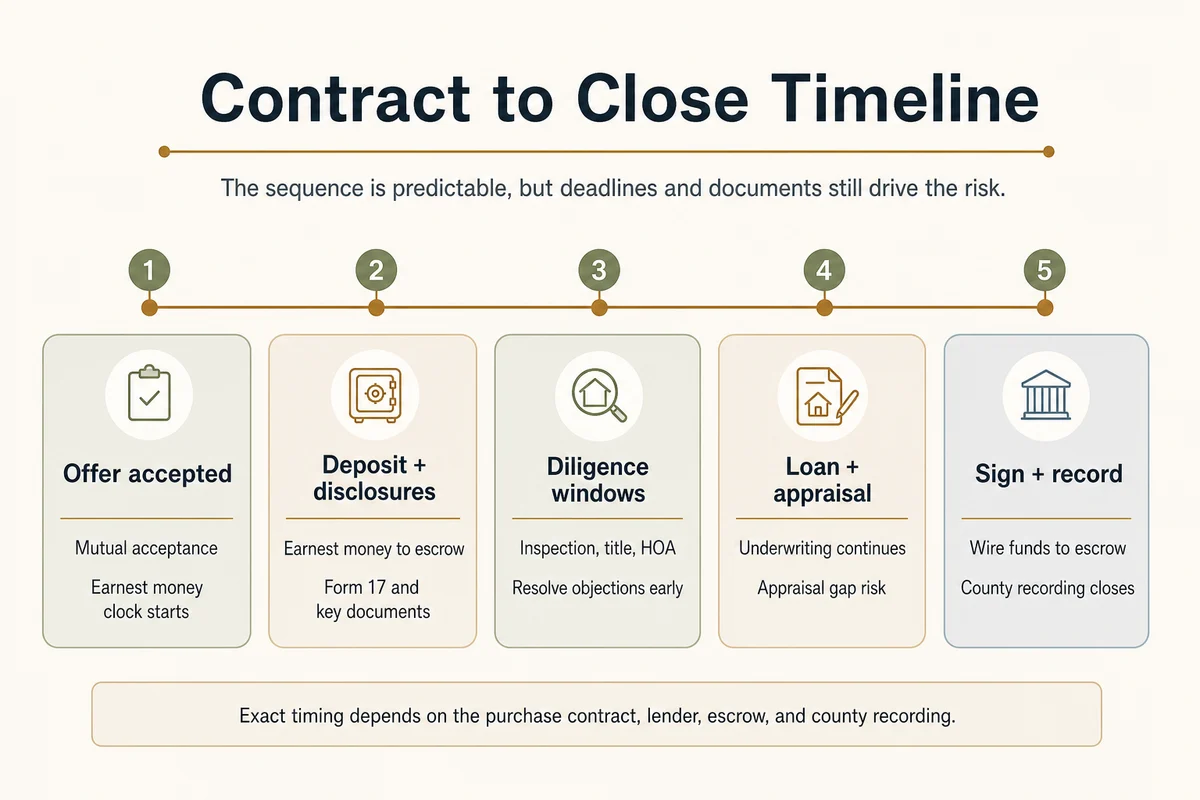

From accepted offer to closing in Washington typically runs 30–45 days. The timeline isn't passive — it's a series of deadlines, each with real consequences if missed.

This article walks through what happens when, what you're responsible for monitoring, and what to expect on and around closing day.

When the clock starts: mutual acceptance

The purchase and sale agreement becomes binding at mutual acceptance — the moment both buyer and seller have signed the same version of the agreement. Every counter-offer and counter-counter-offer resets the clock until both parties have signed identical language.

All contingency deadlines run from mutual acceptance in calendar days. Know this date and write it down.

The earnest money deposit

Shortly after mutual acceptance, per the terms of your agreement, you'll deliver your earnest money deposit to the party named in the contract. In many Washington transactions that holder is escrow or title, but the agreement controls.

The earnest money should not go to the seller directly before closing. It's applied toward your costs at closing. If the transaction closes successfully, it reduces what you owe at closing.

When you keep your earnest money: If you exercise a contingency before its deadline — terminating the agreement during the inspection review period, invoking the financing contingency — your earnest money is returned. Contingencies are the mechanism that protects your deposit while allowing investigation.

When you lose your earnest money: If you terminate the contract after all your contingencies have expired or been waived without exercising them, and no other contractual protection applies, the earnest money typically becomes the seller's liquidated damages. The stakes of contingency management are, in part, the earnest money deposit.

Contingency timeline: the early diligence period

Contingencies are the conditions under which you can exit the contract and recover your earnest money. The specific days are set in your agreement; these are typical ranges.

Inspection contingency

You schedule the home inspection during the review window stated in your contract and complete your review of the report. During the inspection review period, you can:

- Accept the home as-is and remove the contingency

- Negotiate with the seller (ask for repairs, a price credit, or both)

- Terminate the agreement and recover your earnest money

After the inspection contingency deadline passes without termination or extension, the inspection contingency is gone. If you've waived inspection entirely, you have no inspection contingency to exercise.

See waiving inspection in Greater Seattle for when and how this tradeoff is made.

HOA review period (if applicable)

If the property is in an HOA, you receive HOA documents and have a specific review window to examine the CC&Rs, financials, meeting minutes, and resale certificate. See HOA resale certificates for what to look for.

Financing contingency

Your financing contingency protects your earnest money if you're unable to obtain your loan. Before this deadline, your lender needs to issue a formal loan commitment (not just a pre-approval). If the loan falls through before this deadline for reasons within the contingency's scope, you can terminate and recover your earnest money.

After this deadline, you no longer have financing protection. If your loan fails after the financing contingency expires, you may lose your earnest money.

What "financing contingency" protects — and doesn't: The contingency typically covers inability to obtain financing at the terms in your pre-approval (rate type, loan amount, loan program). It generally does not cover changes in your financial situation that you control — losing your job, taking on new debt, making large purchases before closing.

Appraisal contingency

If your offer includes an appraisal contingency, it gives you an exit if the home appraises below the purchase price. Without an appraisal contingency, you're obligated to close at the agreed price regardless of what the home appraises for — and you'd need to bring the difference in cash if the lender won't loan on a price above appraised value.

In competitive markets, appraisal contingencies are sometimes waived or modified. Your agent should explain the specific risk if this comes up in your offer strategy.

The middle period: lending and appraisal

While contingency windows are open, the lender is processing your loan application in parallel.

What you'll receive from the lender:

- Loan Estimate (LE): Within 3 business days of applying, the lender provides this document showing estimated closing costs, rate, and monthly payment. Review it carefully; compare to previous estimates.

- Initial underwriting approval / loan conditions: The underwriter reviews your file and may request additional documentation — pay stubs, bank statements, explanations for deposits, additional information about the property.

- Appraisal: The lender orders an independent appraisal of the property. Timing depends on appraiser availability, property type, lender workflow, and contract timeline. The appraiser visits the property and produces a report comparing it to recent sales. If the appraised value comes in below purchase price, your agent will discuss options with you.

- Clear to close: When underwriting has approved all conditions, you receive clear to close. This is the signal that your loan is fully approved and closing can be scheduled.

What not to do during this period:

- Do not apply for new credit, open new accounts, or take on new debt. This can affect your debt-to-income ratio and potentially delay or jeopardize your loan.

- Do not make large cash deposits without documentation. Lenders need to verify the source of funds; unexplained deposits trigger underwriting questions.

- Do not change jobs. If your employment situation changes, tell your lender immediately — it can affect your qualification.

Closing disclosure and the three-day waiting period

At least three business days before closing, your lender is required to deliver a Closing Disclosure (CD). This document shows your final loan terms, final closing costs, and cash-to-close amount.

Review the Closing Disclosure carefully and compare it to your Loan Estimate. Questions to ask your agent or lender if something looks different:

- Have closing costs increased from the Loan Estimate without explanation?

- Is the interest rate as expected?

- Is the cash-to-close figure consistent with what you planned?

The three-day waiting period after the CD is a federal consumer protection requirement. Closing cannot happen until this period expires unless you waive it in specific circumstances (generally not advisable).

Closing day (recording day) in Washington

Washington is an escrow state. Most buyers never sit across from the sellers. The closing process works like this:

Signing appointment (often the day before or morning of closing day): You sign the loan documents, deed, and other closing paperwork with a notary, often at the escrow company's office. This can also be done remotely with a mobile notary or through remote online notarization. Bring valid government-issued ID.

Funding: After signing, your lender sends the loan funds to escrow, and you wire your remaining cash-to-close amount (down payment minus any credits, plus remaining closing costs). Confirm wiring instructions directly with the escrow company — not through email — to avoid wire fraud. This is one of the highest-risk fraud vectors in real estate transactions.

Recording: The escrow company submits the deed and deed of trust to the county for recording. Recording is the moment title officially transfers. In King County, recording happens electronically and typically occurs the same business day the funds are confirmed.

You receive keys after recording is confirmed — not after signing, not after funds are sent. Until recording is confirmed, the transaction is not technically complete.

After recording: what you'll receive

After closing:

- The recorded deed is mailed by the county to the "return to" address on the document — this is often the escrow or title company, who should then forward it to you. Allow several weeks to a few months. Not all buyers notice receiving it; if you don't receive one, you can obtain a certified copy from the county recording office for a small fee

- Title insurance policies (owner's policy and lender's policy) will be delivered

- Final Closing Disclosure / HUD-1 settlement statement with the official breakdown of all charges

Keep these documents. The HUD-1 may be needed for tax purposes (property tax deductibility varies; consult a tax advisor). The deed and title policy are important records of ownership.