Short answer

Cash to close is everything you bring to the closing table: your down payment, plus the fees, prepaids, and agent costs that go with it.

In Washington state, buyers should budget for total cash needs meaningfully above the down payment alone. The additional amount varies based on loan type, purchase price, lender, closing date, impound setup, HOA fees, and whether the seller offers concessions. Use a rough planning buffer early, but replace it with a written Loan Estimate from your lender and an escrow estimate before you write seriously.

The other thing buyers need to plan for in 2026: buyer agent compensation is no longer automatic. In some transactions, you may need to budget for this separately.

Closing costs vs. cash to close

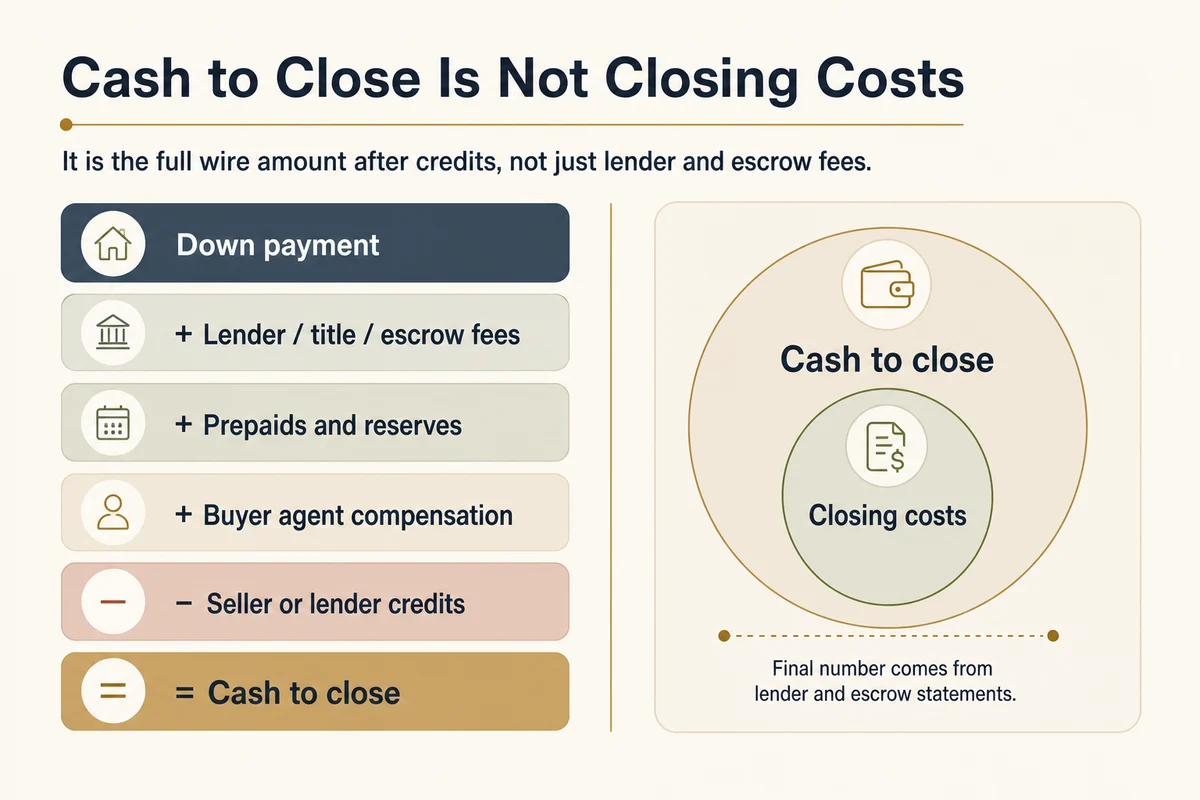

These two terms are often used interchangeably, but they mean different things.

Closing costs are the transaction fees: lender origination fees, title insurance, escrow fees, recording fees, and similar charges.

Cash to close is everything you bring to the table, which includes:

- Down payment

- Closing costs

- Prepaid items (insurance, prepaid interest, property tax impounds)

- Buyer agent compensation (if you're responsible for paying it)

- Minus any seller credits or lender credits you've negotiated

Cash to close is always larger than closing costs alone. Many buyers are surprised when they calculate the full number.

The four buckets

1. Down payment

The largest piece. Common options in Washington:

- 20% or more: No private mortgage insurance (PMI). Conventional loan with straightforward lender requirements.

- 5–19.9%: Conventional loan with PMI until you reach 20% equity.

- 3.5% minimum: FHA loan. More flexible credit requirements, but requires mortgage insurance for the life of the loan (unless you refinance).

- 3% minimum: Some conventional programs (Fannie Mae HomeReady, Freddie Mac Home Possible) for eligible buyers.

- 0% down: VA loans (for eligible veterans and service members) and USDA loans (for eligible rural areas).

Down payment is typically the largest single component of your cash needs. It does not reduce at closing the way some fees can — you bring the full amount.

2. Lender fees

Your lender charges for originating the loan. Common items:

- Origination fee or discount points: Either a flat origination charge or points paid to buy down your interest rate (or both). One point = 1% of the loan amount. Whether paying points makes sense depends on how long you hold the loan.

- Appraisal: Lenders require an independent appraisal of the property. This is typically paid before closing, not at the table.

- Credit report: Usually a small, one-time fee.

- Underwriting fee: Some lenders charge separately for underwriting; others bundle it into origination.

Your lender is required to give you a Loan Estimate within three business days of your loan application. This document breaks out every lender fee category by line item. Use it to compare lenders — the same APR from two different lenders can have very different fee structures.

3. Title, escrow, and recording

Washington uses escrow companies (often also functioning as title companies) to handle the closing process.

Owner's title insurance: A one-time premium that protects your ownership rights against title defects. In Washington, it's customary for the seller to pay for the owner's policy, though this is negotiable. Lender's title insurance (protecting the lender's interest) is almost always a buyer cost.

Escrow fee: The escrow company charges for managing the closing — holding funds, coordinating documents, processing the transaction. Both buyer and seller typically share this cost, though the split is negotiable.

Recording fees: King County and other counties charge fees to record the deed and deed of trust. These are a buyer cost.

Excise tax: Washington's real estate excise tax (REET) is a seller cost, not a buyer cost. Buyers do not pay excise tax.

4. Prepaids and reserves

These are often the most confusing part of cash to close because they're not "fees" — they're payments made in advance.

Prepaid homeowners insurance: Your lender will require homeowners insurance to be paid before or at closing. This is typically a full year paid upfront, plus two months escrowed.

Prepaid interest: From the closing date to the end of the month. If you close on May 21st, you prepay interest for the days from the 21st to May 31st, then your first regular payment covers June.

Property tax impounds: If your loan requires an escrow account, your lender will collect several months of property taxes upfront to fund the impound account.

The total of prepaids and reserves can be several thousand dollars depending on property tax amounts, insurance premiums, and closing date timing.

Buyer agent compensation: what changed in 2024

Before August 2024, sellers in most markets automatically offered buyer agent compensation through the MLS. Buyers typically paid nothing directly to their agent.

After the NAR settlement changes took effect in Washington:

- Buyer agent compensation is no longer offered or advertised through the MLS.

- Sellers may still offer a concession that the buyer can apply toward their agent's fee — but it must be negotiated separately.

- Buyers sign a buyer brokerage agreement before touring homes that specifies what they will pay their agent if the seller does not cover it.

What this means practically:

- Some Washington sellers still offer buyer agent concessions because doing so can attract more buyers with broader financing options.

- But not all do. If a seller offers no concession, the buyer is responsible for paying their agent directly — this goes through escrow and appears on your closing statement.

- You should understand your buyer brokerage agreement's compensation terms before writing an offer, and factor it into your cash-to-close estimate.

This is a legitimate budget item for buyers in 2026. Plan for it; don't assume the seller will cover it.

Seller credits and how they reduce your cash

If market conditions allow, you can negotiate a seller credit toward your closing costs and prepaids. This reduces the cash you bring to closing.

A few things to know:

- Seller credits generally cannot be applied toward your down payment — they offset allowable fees, prepaids, and other lender-approved costs.

- There are caps and program rules on how much a seller can contribute toward buyer costs. Conventional, FHA, VA, and portfolio loans handle these differently.

- Fannie Mae has clarified that seller-paid real estate agent fees may be treated differently from ordinary Interested Party Contributions when they are customary for the transaction, but lender interpretation still matters. Do not assume every credit can be used the same way.

- A credit that exceeds what your lender allows will be reduced or unused, not pocketed. Budget conservatively.

- Seller credits are more commonly available in slower markets or with homes that have been sitting. In a competitive multiple-offer scenario, asking for a large seller credit may weaken your offer.

Common cash-to-close surprises

Escrow timing: In Washington, you wire funds to escrow before the closing date — usually one to two days before recording. Make sure your funds are in an accessible account and you've done a test wire if your bank imposes daily transfer limits.

Rate lock expiration: If your closing is delayed and your rate lock expires, you may need to pay for a lock extension. This adds to your cash needs unexpectedly.

HOA setup fees: Some HOA-managed properties charge a move-in fee, transfer fee, or reserve deposit at closing. This typically appears on the closing statement.

Earnest money credit: Your earnest money deposit is applied toward your cash to close at funding. It doesn't disappear — it offsets what you wire at the end. But you need to have it available at the beginning of the transaction too.

How to estimate your number before making an offer

A useful pre-offer cash estimate:

- Calculate your down payment based on your target purchase price and loan type.

- Ask your lender for an early cash-to-close worksheet for everything except the down payment: lender fees, title, escrow, prepaids, and impounds. Your Loan Estimate will replace rough planning assumptions with actual line items once you apply.

- Factor in buyer agent compensation based on what's in your brokerage agreement and what you expect the seller to offer in this specific transaction.

- Subtract any seller credit you plan to negotiate.

- Add a buffer of a few thousand dollars for items that come in higher than expected.

This is a rough estimate. The Loan Estimate from your lender — which you should get before you're deep into a specific transaction — will give you actual line-item numbers.