Short answer

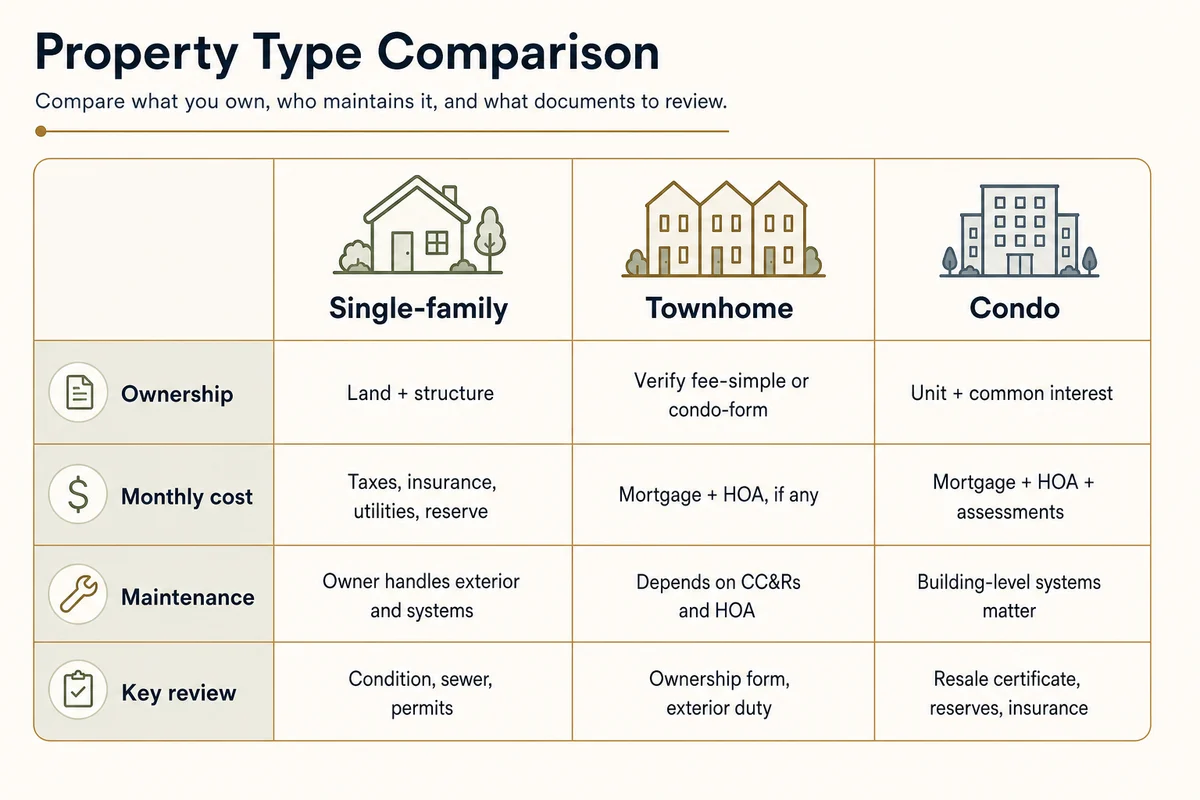

Choosing between a single-family home, townhome, and condo is not primarily a question of what looks best or what has the most space — it is a question of what you own and what that ownership costs each month.

In Greater Seattle, all three property types exist across a wide range of prices, locations, and conditions. The right comparison is not category vs. category but rather this specific property's total monthly cost, ownership structure, maintenance exposure, and how it fits how you actually live.

This is not a ranking

Single-family homes are not always the best choice. Condos are not always a stepping stone. Townhomes are not universally "the best of both worlds." Every version of that framing overgeneralizes.

This comparison gives you the framework to evaluate a specific property — what to verify, what questions to ask, and what tradeoffs matter most depending on your situation.

First: confirm what you are actually buying

The most common mistake in this comparison is treating "townhome" as a consistent ownership type. It isn't.

The word "townhome" describes a physical style — multi-story, usually attached, often with stairs. It says nothing about how the property is legally organized. A townhome in Greater Seattle may be:

- Fee-simple: You own the land and the structure outright. No HOA, or a minimal one with no shared building components.

- Condo-form: The property is organized as a condominium, even if it looks like a townhome. You own your unit; the HOA owns and maintains shared elements like roofs, siding, and exterior systems.

- PUD (Planned Unit Development): A hybrid structure where you own the lot and structure but share common areas through an HOA.

This distinction matters enormously for maintenance responsibility, HOA dues, financing requirements, and resale. Verify the ownership form — not the building style — before you make any comparison.

| Ownership Form | Land | Structure | HOA Typical Role |

|---|---|---|---|

| Fee-simple | You own it | You own it | Optional or minimal |

| Condo | Common area share | Unit only | Owns exterior, roof, systems |

| PUD | You own it | You own it | Maintains common areas |

What each property type means in practice

Single-family home (SFH)

A detached house, typically with its own lot. Most SFHs in Greater Seattle are fee-simple — you own land and structure.

What you control: You can renovate, paint, add a deck, plant or remove landscaping, and in many cases build an ADU or DADU, subject to zoning and permit requirements.

What you're responsible for: Everything. Roof, exterior, siding, drainage, foundation, HVAC, sewer line, landscaping, and any repairs. There is no HOA to call.

Daily-life tradeoff: You get the most autonomy and usually the most private outdoor space, but you also own the time burden. Yard work, drainage, moss, trees, pests, and exterior repairs either become weekend projects or contractor invoices.

Who it usually works for: Buyers who want autonomy, value private outdoor space, have a longer time horizon, and are prepared to take on maintenance.

Townhome

A multi-story attached unit, usually sharing at least one wall with a neighbor.

What you control: Depends entirely on ownership form. A fee-simple townhome gives you full control of structure and lot. A condo-form townhome means exterior maintenance and major systems are the HOA's job — but also their decision.

What you're responsible for: Varies. In a condo-form townhome, you typically maintain the interior; the HOA handles roof, siding, and exterior systems. In a fee-simple townhome, you handle everything, even if there is a common area HOA for shared driveways or landscaping.

HOA dues: Verify what they actually cover. Dues that look low may reflect deferred maintenance, thin reserves, or an HOA that leaves more to individual owners.

Daily-life tradeoff: Townhomes can offer more usable space than many condos without the full yard burden of a detached house, but stairs, shared walls, limited guest parking, and small or absent outdoor areas affect daily use.

Who it usually works for: Buyers who want more space than a condo with less maintenance exposure than a detached SFH — but the fit depends heavily on the specific unit's ownership form and HOA health.

Condo

A unit in a larger building or development. You own the interior of your unit; the HOA owns and manages the building exterior, roof, common areas, and shared systems.

What you control: Less than an SFH or fee-simple townhome. Most condos require HOA approval for significant interior changes, limit rental use, and restrict exterior modifications entirely.

What you're responsible for: Usually your unit interior, finishes, fixtures, and appliances, but the boundary between owner responsibility, limited common elements, and association responsibility must be verified in the declaration and resale certificate. Do not assume every pipe, window, deck, or wall component is the HOA's job.

HOA dues: Typically higher for condos than for fee-simple townhomes, because they cover more. A condo with high dues may actually be a better deal than one with low dues if the higher dues reflect adequate reserves and comprehensive coverage.

Financing: Condos require the building to be on a Fannie Mae or FHA approved list, or go through spot approval. Buildings with high investor ownership, pending litigation, or underfunded reserves may not qualify for standard financing. Verify warrantability before going under contract.

Daily-life tradeoff: Many condos put you closer to restaurants, transit, gyms, pools, concierge services, or entertainment than a comparable detached home budget would. For some buyers, that shared-building lifestyle feels more connected and convenient than a quieter detached-home setting farther out.

Who it usually works for: Buyers who prioritize location, walkability, amenities, or lower exterior-maintenance responsibility, and who are comfortable with shared building governance.

Monthly cost comparison: what to actually calculate

List price is not a useful comparison. Monthly cost is.

For a single-family home, the relevant costs are: principal and interest, property taxes, homeowners insurance, and the ongoing maintenance and repair budget you set aside. There is typically no HOA.

For a condo, add HOA dues to the above — and understand that dues can increase. Also factor in special assessments: one-time charges levied when reserves are insufficient to cover a major repair.

For a townhome, the calculation depends on ownership form. A condo-form townhome works like a condo. A fee-simple townhome with a nominal HOA works more like a single-family home.

Don't compare:

- A condo's list price to an SFH's list price without accounting for HOA dues, reserve health, and what the HOA covers.

- A "low HOA" condo to an SFH's maintenance burden without verifying what the HOA defers.

Do compare:

- All-in monthly cost: PITI + HOA + a realistic maintenance/reserve estimate for the specific property.

- What the HOA actually covers and what its reserves can absorb without a special assessment.

The HOA resale certificate is the document that answers most of these questions for condo and HOA-organized townhome buyers.

Financing differences

Single-family homes and fee-simple townhomes generally have no property-level financing restrictions. Lender approval is about your financial qualifications, not the building.

Condos must meet the project standards for the loan program being used. A project-level issue such as insufficient insurance, pending litigation, budget or reserve concerns, high investor concentration, or other guideline problems may require different financing or a different loan product.

If you are considering a condo, ask your lender to verify warrantability before you go under contract. A failed warrantability check late in the transaction can mean renegotiating your financing or losing your earnest money if you don't have a financing contingency.

For new construction condos, Fannie Mae has additional requirements for newly created common-interest communities. Ask your lender about pre-sale or project approval requirements.

Noise, privacy, and layout

Single-family homes generally offer the most physical separation from neighbors. Noise transmission depends on lot size and proximity, not a shared wall.

Townhomes share at least one wall, and sometimes a floor/ceiling depending on configuration. Sound transmission through shared walls and stairs is a common quality-of-life consideration. Visit the specific unit at different times of day if possible.

Condos often share walls, floors, and ceilings. Building construction type (wood-frame vs. concrete) and the specific unit's position within the building affect noise levels significantly. A top-floor, corner unit in a concrete building has different noise exposure than a middle-floor unit in a wood-frame building.

Resale: what to verify for each type

Rather than making category-level claims about liquidity, focus on what to verify for the specific property:

Single-family homes: Check how comparable homes in the same area have transacted recently, what the dominant buyer profile is, and whether the lot or structure has characteristics that narrow the buyer pool (unusual lot size, hill-climbing access, minimal parking, or a layout that doesn't work for the most common buyers in that submarket).

Condos: Buyer pool can be affected by building financing status (non-warrantable condos have a smaller buyer pool), rental restriction trends (restrictive rental policies reduce investor buyer demand), and building condition and reserve health. A well-run condo in a warrantable building tends to have a broader buyer pool than a building with known issues.

Townhomes: Resale depends on whether future buyers understand and accept the ownership form you have. A fee-simple townhome with practical layout, parking, and clear maintenance responsibility is a different product from a condo-form townhome with unresolved HOA or reserve issues.

For a more detailed look at how these two property types specifically compare in Greater Seattle, see Seattle Condo vs. Eastside Townhome.

Questions to ask yourself

Before using this comparison:

- What does "townhome" mean for this specific property? Fee-simple or condo-form — verify from public records or the listing disclosure, not the marketing description.

- What is the HOA's reserve fund balance relative to what it needs to maintain? A reserve study tells you. An underfunded reserve is deferred cost.

- What is my realistic all-in monthly cost at this price and rate, including HOA and a maintenance budget?

- Does this property's ownership structure and location fit how I actually plan to live and for how long?

- If I want to finance with a conventional loan: is this condo warrantable?